Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

Predictive density of σ T +1 for EGARCH model, GJR model and Bayesian ...

egarch - EGARCH conditional variance time series model - MATLAB

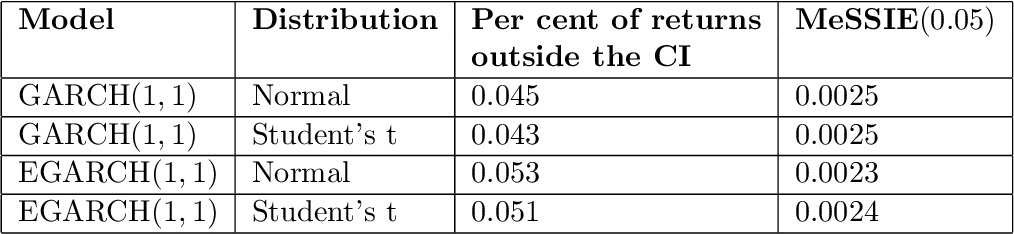

Estimation results of EGARCH model with normal and student's t ...

Conditional Variance EGARCH Model | Download Scientific Diagram

Egarch Model | PDF | Null Hypothesis | Normal Distribution

Regression results with an EGARCH model of the conditional variance ...

AIC/SIC result from the initial EGARCH model | Download Scientific Diagram

Result of EGARCH (1, 1) and TARCH (1, 1) Model | Download Scientific ...

Results from the GARCH model, the EGARCH model and the ECM with GARCH ...

Estimation of EGARCH model under the full sample | Download Scientific ...

Asymmetric EGARCH Model for different indices Panel A: Volatility of ...

Conditional variance of EGARCH (1, 1) model (see online version for ...

(PDF) Improving Value-at-Risk Estimation from the Normal EGARCH Model

Conditional standard deviation of EGARCH (1, 1) model (see online ...

(PDF) Egarch Model Prediction for Sale Stock Price

Estimation of The Egarch Model For All-share Index As The Dependent ...

Estimation of the EGARCH model with different distributions. | Download ...

Diagnostic test of the GARCH (1,1), EGARCH (1,1) and TGARCH (1,1) model ...

The Estimation Results of EGARCH Model | Download Scientific Diagram

Estimates of the GARCH and EGARCH model for the DAX GARCH EGARCH ...

EGARCH Model Results (Including WALSIN) | Download Scientific Diagram

EGARCH Model Panel A: Volatility of Nifty & BSE30 after Introduction of ...

Maximum likelihood estimation of EGARCH model (with mean and without ...

Relation between Market Return, Volatility and Volume by EGARCH Model ...

Estimation results for EGARCH model with MA specification. | Download Table

Figure 1 from Improving Forecasts of the EGARCH Model Using Artificial ...

Maximum likelihood estimation of EGARCH model (with mean and time trend ...

Estimated parameters and associated standard errors in the EGARCH model ...

Specify EGARCH Models - MATLAB & Simulink

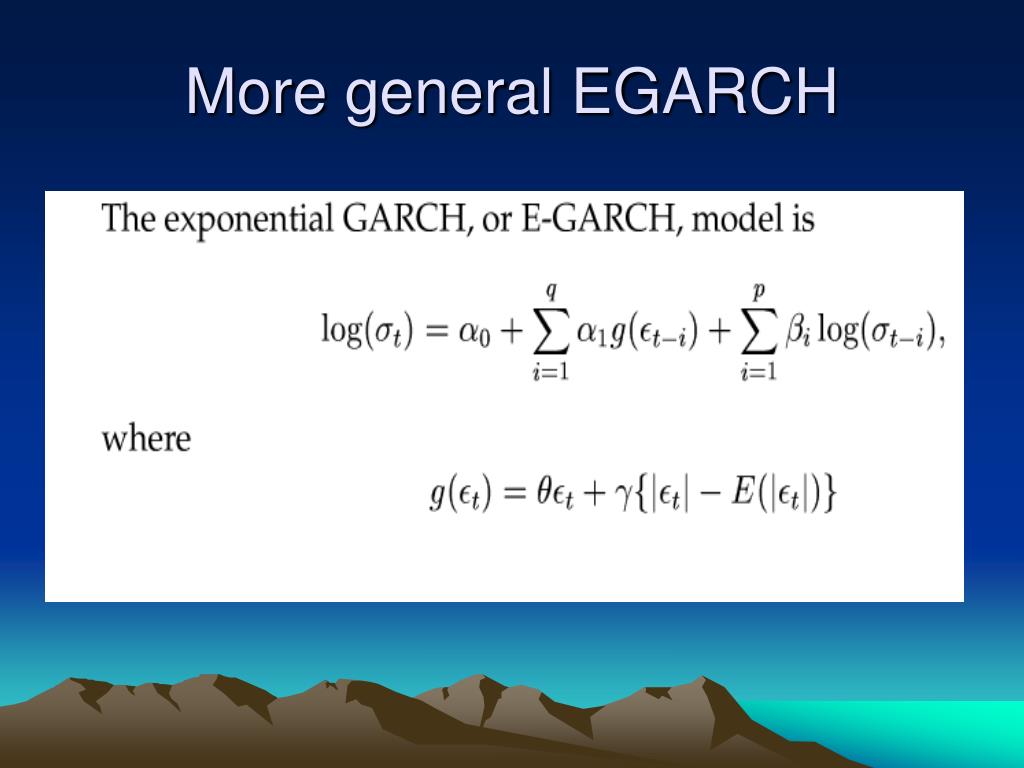

PPT - THE EXPONENTIAL GARCH MODEL PowerPoint Presentation, free ...

PPT - Week 10: VaR and GARCH model PowerPoint Presentation, free ...

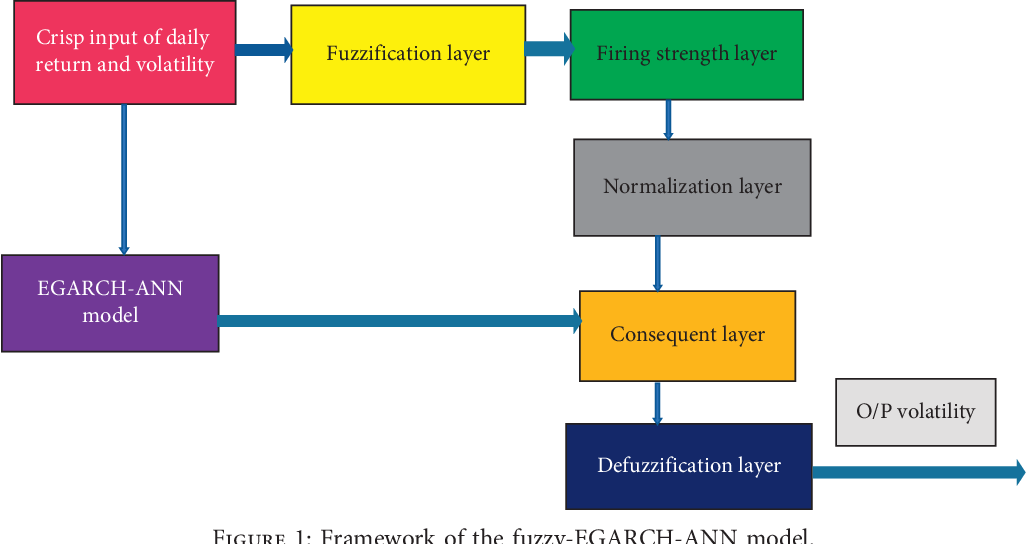

Architecture of the fuzzy-EGARCH-ANN model with p = 1, q = 1, m = 1 ...

Conditional Standard Deviations of GARCH and EGARCH Models | Download ...

EGARCH model: exponential asymmetric volatility persistence (Excel ...

Estimated parameters APARCH, TGARCH, and EGARCH model. | Download ...

Results of the estimation of the EGARCH(1,1) model with the slope in ...

Estimation Statistics-Distribution Comparison AR(1)-EGARCH Model ...

Regression results of EGARCH (1,1) and TGARCH (1,1) | Download ...

Volatility and Asymmetry Effects, Estimated Co-efficients of the EGARCH ...

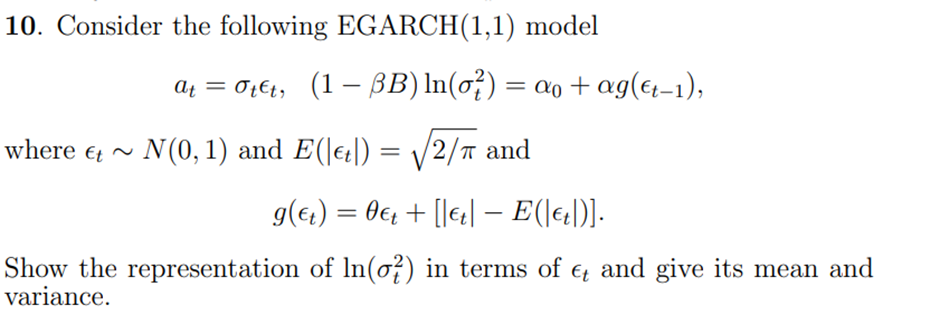

Solved 10. Consider the following EGARCH(1,1) model a_t = | Chegg.com

(continuation). Forecast comparison in the sample of the EGARCH (1, 1 ...

EGARCH Model: Daily Data | Download Table

Comparison of Garch and Egarch Models | Download Scientific Diagram

Estimation results of GJR-GARCH and EGARCH models with contemporaneous ...

EGARCH(1,1) Model Evaluation depending on Information Criteria and ...

Estimations for GARCH and EGARCH models | Download Scientific Diagram

Inflation volatility graph of EGARCH ( 1,1 ) model. | Download ...

Empirical results of the EGARCH (1, 1) and GARCH models. | Download ...

Relationship between epochs and loss in the hybrid model of GARCH ...

Estimated EGARCH models: Variance equation. | Download Scientific Diagram

Flowchart for calibration and validation of EGARCH and EGARCH-ANN ...

Figure2:The implied volatility of the GJR-GARCH and EGARCH calibrated ...

Variation of dynamic correlation coefficient of DCC-EGARCH model ...

Estimation Outputs of Multifactor GARCH, TGARCH and EGARCH Models ...

Egarch Model: The Indian Institute of Planning & Management, AHMEDABAD ...

EGARCH(1,1) Model without dummy variables | Download Table

Estimated volatility by the GARCH(1,1) model | Download Scientific Diagram

EGARCH volatility estimates and ETF investment size | Download ...

Statistics for EGARCH and TGARCH Parameters for both Periods | Download ...

Parameter Estimates of CC-EGARCH Model | Download Table

CCC-VAR-EGARCH Model with Spillover and Asymmetry | Download Table

Can an EGARCH model's coefficients be used to conclude the effect of ...

Table 1 from The volatility of tomorrow-Comparison of GARCH and EGARCH ...

EGARCH Process For Determining The Exchange Rate Volatility | Download ...

Задайте модели EGARCH

Results of the EGARCH and GJR-GARCH Models | Download Scientific Diagram

Diagnostics statistics -Distributions Comparison AR(1)-EGARCH Model ...

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

PPT - Chapter 8 PowerPoint Presentation, free download - ID:3966639

PPT - Democratic Politics and Financial Markets PowerPoint Presentation ...

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch # ...

PPT - 國際天然氣市場的訊息傳遞與價格互動 PowerPoint Presentation - ID:5064728

ARCH and GARCH. Modeling Volatility Dynamics - online presentation

PPT - Lecture 8: Conditional Heteroscdastic Models PowerPoint ...

The likelihood values of (a) GARCH, EGARCH, and GJR-GARCH models; (b ...

Solved Problem 4. (EGARCH(1,1) model)The exponential GARCH | Chegg.com

GARCH、GARCH-M、IGARCH、TARCH、EGARCH、PARCH、CGARCH模型-操作视频地址大全财经节析-张华节-计量经济学 ...

How to interpret the resulting coefficients in the conditional variance ...

Volatility Modeling (part 1): Journey from ARCH to NN and MCMC

25. Estimating ARCH and GARCH models using EViews (Part-2)||ARCH, GARCH ...

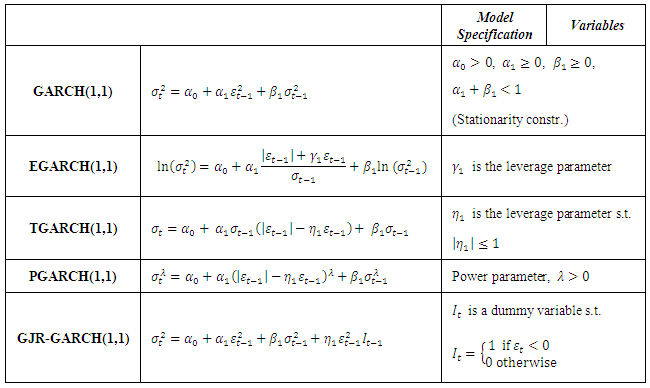

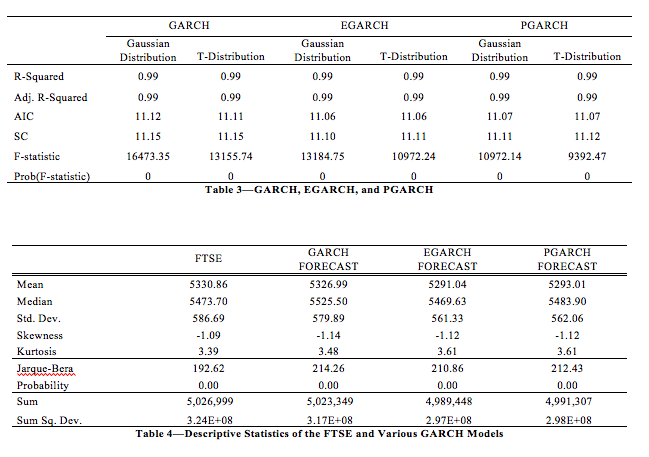

GARCH, IGARCH, EGARCH, and GARCH-M Models

How to interpret negative ARCH coeff. and positive leverage effect ...

(PDF) Modeling Exchange Rate Volatility: Application of the GARCH and ...

GitHub - mwangiian/GARCH-ARCH-TARCH-EGARCH-models: In econometrics, the ...

Conditional variance from EGARCH(1,1) Model. | Download Scientific Diagram

Forecasting USD/MUR Exchange Rate Dynamics: An Application of ...

Sample | Volatility Modelling and Forecasting Using GARCH

Graph dependency for KLCI-FBMHS pair using a) ARMA-GARCH models and b ...

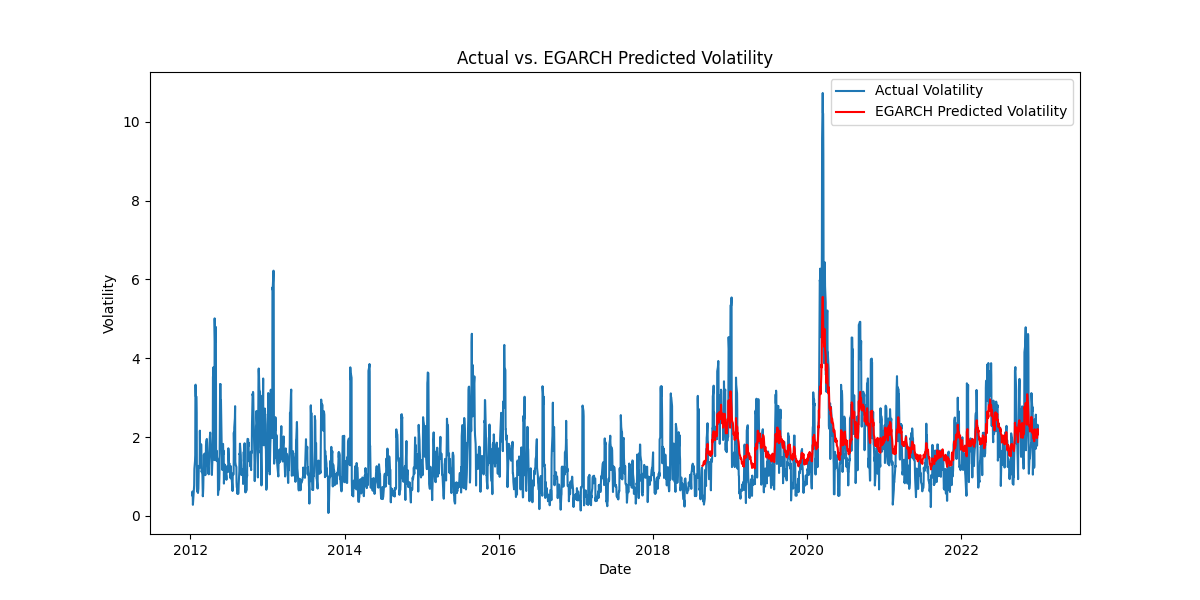

Comparison of realized volatility and conditional volatility (EGARCH ...

GitHub - DavidAlexanderMoe/Financial-Time-Series-Analysis-and ...

Parameters Estimation EGARCH(1,1) | Download Scientific Diagram

(EViews10): How to Estimate Standard GARCH Models #garch #arch # ...

(PDF) Modelling and Forecasting of Price Volatility: An Application of ...

Figure 1 from Modeling and Forecasting Stock Market Volatility by ...

EGARCH: estimated coefficients of the conditional volatility equation ...

Summarized results of OLS, GARCH(1,1) and EGARCH(1,1) models | Download ...

Know the Basics of ARCH Modeling (Part 1)#arch #volatility #modeling # ...

Results of Conditional Volatility of Natural resources rents derived ...

Results of the Volatility Models | Download Scientific Diagram

presents the empirical results of the AR-EGARCH model. As shown in this ...

EGARCH: un modelo asimétrico para estimar la volatilidad de series ...

EGARCH(1,1) Variance Estimates | Download Scientific Diagram

Estimation Results. ARMA-EGARCH Model. The table shows the results of ...

(PDF) Modelling and Estimation of Volatility Using ARCH/GARCH Models in ...